There is no greater movement within the traditional operational business units and functions of consumer products manufacturers and suppliers than with the revenue growth management organization. We asked 298 consumer products executives about their RGM practices and organizations, and especially about their role in the annual integrated business planning process. They had a lot to say!

For the past few years at least, the position of the revenue growth management function and role within so many consumer products companies is dramatically changing. RGM is a topic that is top of mind and agenda across the greater consumer industries.

Recent event gatherings across the industry have included topics around RGM and certainly generated significant networking chatter among attendees. Formal surveys and state-of-the-industry publications have projected RGM to be one of the most active organizational reengineering topics in their analyses.

In the research for my book, “The Invisible Economy of Consumer Engagement,” so much of what was learned was that the RGM role is expanding in responsibility with its leadership rising up the corporate command chain. The feeling among the people I interviewed is that the practical reasoning for this elevation in function and corporate leadership position is that there is a need for a consolidation of every aspect of the corporate value chain that contributes to the generation of revenue.

Building the Modern RGM Practice

Building the Modern RGM Practice

In the research we conducted, we found out that there was visible change happening in the RGM function in 70% of the companies we surveyed.

We have seen a vigorous reorganization among many major consumer products companies to include more direct control of the most impactful activities that directly lead to revenue generation, including trade and channel promotion and retail execution. In fact, almost one-third (31%) of those companies said major changes were happening to their RGM business units.

We also know that many consumer products companies are elevating the role of leadership for RGM to executive vice president and even to the C-suite (e.g., Chief Revenue Officer).

This clearly signals a change in the perception of corporate leadership of the importance of this operational transformation to one that has high priority and increased respect for the roles and responsibilities of the entire RGM team.

Of the nearly 300 manufacturers we spoke with, 34.5% indicated that the leadership of RGM was now at least an EVP, with almost 5% of that number in the C-Suite.

This is a significant change, and again, shows that the functional value of RGM has validated what so many consumer products executives, analysts and trade media has pushed for decades.

“We believe that, while our operating units have all been very strong in calculating their individual BU plans, forecasts and financial expectations, there was too much independent execution,” says the CFO of a global CPG conglomerate. “It’s time for us to make the commitment to RGM as a priority, and to equip our CRO with the tools and talent she needs to make sure we have a solid plan we all march to.”

This feeling is shared among virtually all of the executives we polled; but we also know that the political situation within both large and small companies can impede the progress and throw a spanner in the works if there is no respect for the RGM leadership. The persons being placed in charge of these expanded and elevated RGM units are going to be facing significant challenges to their ability to succeed.

This feeling is shared among virtually all of the executives we polled; but we also know that the political situation within both large and small companies can impede the progress and throw a spanner in the works if there is no respect for the RGM leadership. The persons being placed in charge of these expanded and elevated RGM units are going to be facing significant challenges to their ability to succeed.

Not unexpected, the top two overwhelming responses to the question of challenges were data and technology. Data issues are still a major problem for virtually all consumer products companies, as they are for retailers and wholesaler/distributors as well.

Also not surprising was nearly one-third of the respondents concerns over cross-organizational collaboration. This is especially true for companies where the new RGM chief is being given the responsibility to lead the collaboration between key value chain teams such as supply chain, manufacturing, procurement, marketing, logistics and of course, IT.

22.8% of the respondents felt that finding and employing solid talent was going to be a challenge, because now, the concentration of data and analytics covers all of these other value chain organizations and dealing with them will demand a very special set of core competencies.

“The job descriptions we have to write are now far more complex, and it is almost like hiring a CEO of a small startup,” says the HR director for a leading automotive aftermarket company. “It’s not just the functional duties, but also the combination of focusing on a revenue generation outcome and political sensitivity!”

Expanding the Functional Scope of RGM

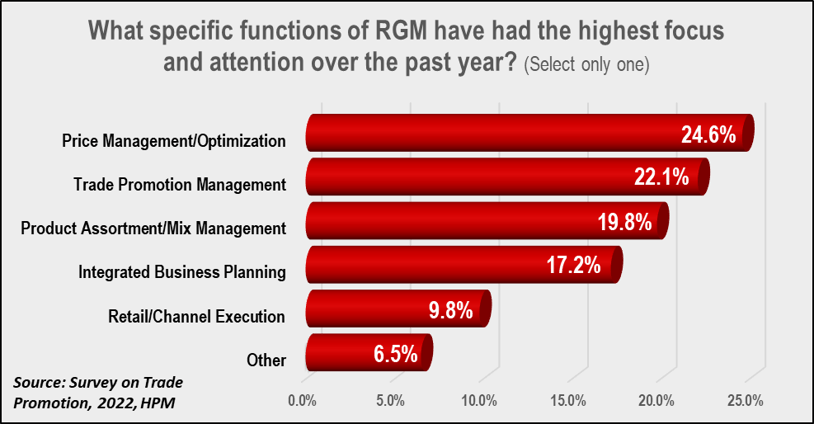

Traditionally, RGM has focused on price management, product mix and channel assortment—the right product at the right price.

What we see coming is a top down reengineering of the RGM business unit to combine functions that are typically under the sales, marketing, or operations units. Straight line reporting relationships now include trade promotion management, retail execution and expanded cross-functional analytics.

Surprisingly, however, the responsibility of RGM for the management of the integrated business planning process (the formal annual financial and value chain planning for consumer products companies) was selected by over 17% of the respondents. This process is usually led by finance, so this represents a new direction for companies that hope to broaden the focus on P&L to incorporate more emphasis on both operations and consumer engagement.

Surprisingly, however, the responsibility of RGM for the management of the integrated business planning process (the formal annual financial and value chain planning for consumer products companies) was selected by over 17% of the respondents. This process is usually led by finance, so this represents a new direction for companies that hope to broaden the focus on P&L to incorporate more emphasis on both operations and consumer engagement.

What is even more surprising, however, is that for the 137 fast moving consumer goods companies on the survey, the responses showed even higher percentages for trade promotion management and IBP functional process ownership at 27.1% and 19.3% respectively.

Dotted line reporting relationships with RGM have also increased for marketing, IT, finance, and procurement as well. Supply chain, especially demand planning, has always been tightly aligned with RGM planning and analytics, so little has changed there.

The Importance of Integrated Business Planning (IBP)

Supply chain management guru Oliver Wight coined the term “IBP” as the next logical evolution of another process he created, supply and operations planning (S&OP) back in the 1980s. Not to promote a specific product or brand, but one of the better articles on IBP is on Oracle’s NetSuite site (HERE). Check it out.

The article has it right by stating that IBP is now a highly charged corporate process. Our survey clearly supported the acceleration of interest in IBP and how to leverage the process to not only convert the corporate financial and P&L plan to operational execution, but to enable ongoing action when any aspect of the plan goes awry.

We asked the 298 respondents about what they perceived as the top barrier to effective planning. Again, unsurprisingly, issues with data and the technology to clean, harmonize, align and analyze ranked as the top issues.

We asked the 298 respondents about what they perceived as the top barrier to effective planning. Again, unsurprisingly, issues with data and the technology to clean, harmonize, align and analyze ranked as the top issues.

Product issues were cited next, which includes factory production, materials procurement, category and brand mix as well as assortment planning. New product launches and failures were also included in the definitions of this barrier.

As with any committee, not everyone agrees unanimously with corporate strategic objectives and goals. One in ten respondents argued that time taken to work through the cross-organizational views and opinions of corporate strategy and tactics contributed to the lengthy  nature of IBP and often ended without consensus on direction, but at least agreement to embrace and execute against the strategic plan.

nature of IBP and often ended without consensus on direction, but at least agreement to embrace and execute against the strategic plan.

Speaking of lengthy timeframes for IBP, we asked specifically how long companies took from the first activity to the final agreed plan.

90% of the respondents said their IBP process took at least 6 weeks, with almost 40% saying between 8 and 12 weeks and almost 20% taking longer than 12 weeks.

Breaking down the numbers even further, we noted that most of the responses fell into the higher end of the timeframe.

- 8 – 12 Weeks: 8 – 10 weeks = 22%; 11 – 12 weeks = 78%

- 6 – 8 Weeks: 6-7 weeks = 38%; 8 weeks = 62%

As stated earlier, the traditional ownership of the IBP process has been primarily finance, but that seems to be changing as well. The question of what organization is the primary owner of the IBP process gained almost 100% response by the survey universe.

More than one-third (34.1%) responded that finance is the outright owner of the IBP process. Within FMCG only, by the way, that figure jumps to 41%.

More than one-third (34.1%) responded that finance is the outright owner of the IBP process. Within FMCG only, by the way, that figure jumps to 41%.

29.5% responded that IBP initiatives were shared ownership, as you see the breakdown in the chart. But also consider that 9.3% of the respondents tagged RGM as the outright owner of the IBP process. If you look at the shared ownership figures, note that RGM is one of the co-owners in another 12.5% of the companies, giving RGM all or part ownership of the IBP process in 21.8% of the companies polled.

RGM Rising

Its’ almost a “duh” statement now, but the importance of RGM becoming a central control point for so much of the critical operational functions says a lot about the future of planning across all consumer products companies. The elevation of leadership of RGM to EVP and C-levels within the organization signals an intention to streamline and align all planning functions to achieve a more accurate and timely operating and financial plan.

But with ownership of trade promotion, retail execution and expanded dotted line relationships with marketing and demand planning, does it also imply a higher, more intense focus on the consumer?

It should.